AP Microeconomics : AP Microeconomics

Study concepts, example questions & explanations for AP Microeconomics

All AP Microeconomics Resources

Example Questions

Example Question #1 : Microeconomics Graphs

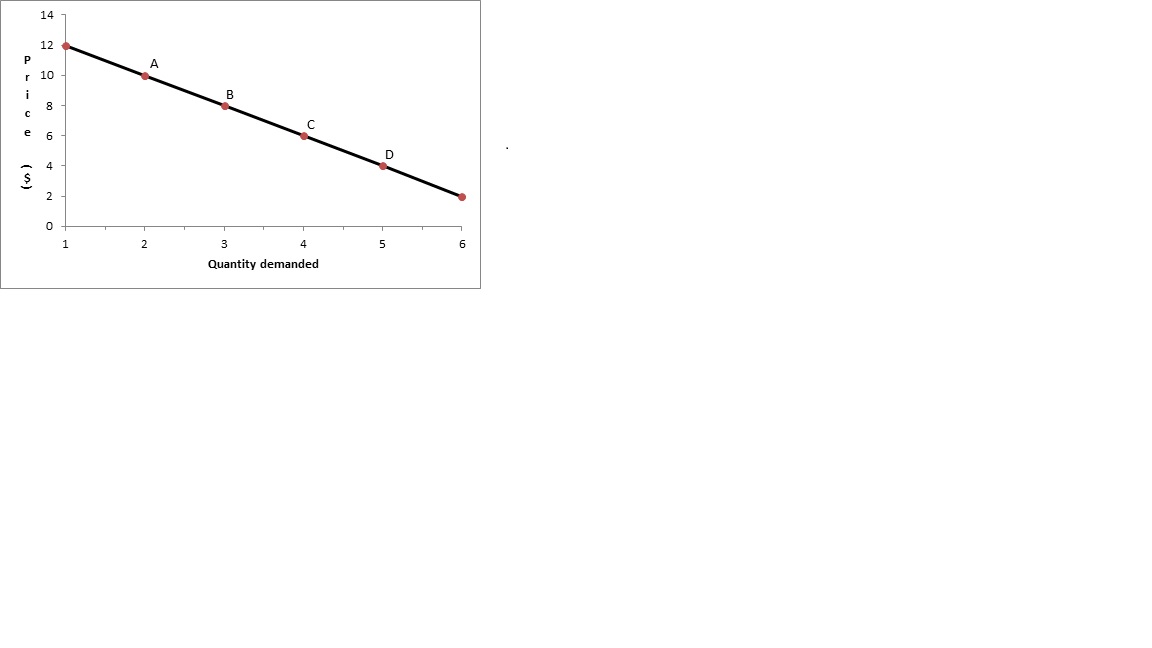

The demand for oranges at point D is:

Unit elastic

Inelastic

Perfectly elastic

Elastic

Perfectly inelastic

Inelastic

For a demand curve, the upper left portion is elastic, the middle portion is unit elastic and the lower right portion is inelastic. You can confirm by calculating E = percent change in quantity/ percent change in price between the points on the lower right portion of the demand curve. If E < 1, then demand is inelastic.

Example Question #1 : Microeconomics Graphs

Suppose a consumer finds that her total expenditure on good X increases after her income decreases. Which of the following is true?

The income elasticity of good X for the consumer is 1.

Good X is a normal good for the consumer.

Good X is a luxury good for the consumer.

Good X is an inferior good for the consumer.

Good X is an inferior good for the consumer.

When a consumer buys less of a product after a rise in income, the good is said to be an "inferior good." (Consider, for example ramen noodles--for most consumers, when income rises, they purchase fewer ramen noodles).

Another way to think about inferior goods it that the income elasticity is negative. The formula for income elasticity is change in quantity demanded divided by change in income. In the scenario in question, income rose (so the denominator, change in income, is positive), and the quantity demanded fell (so the numerator, change in quantity demanded, is negative). Thus, the income elasticity would be negative, making good X an inferior good.

Good X is not a normal good, because for normal goods, income elasticity is between 0 and 1 (not negative).

Good X is not a luxury good, because for luxury goods, income elasticity is greater than 1 (not negative).

The income elasticity of good X for the consumer is not 1, because we know from the explanation above that income elasticity for good X must be negative.

Example Question #1 : Price

Assume that a consumer is willing and able to pay $5 for a latte and that the price of the latte is $3. Which of the following is equal to the consumer surplus?

$8

$2

$15

$1

$2

Consumer surplus is calculated as the amount a buyer is willing and able to pay for a good or service minus the actual cost of the good or service. Thus, if the consumer is willing and able to pay $5, but the good costs only $3, consumer surplus is $5 - $3 = $2.

Example Question #2 : Microeconomics Graphs

Suppose that as result of a 10% increase in income, the quantity demanded of Good X increases by 20%. Which of the following is true?

The income elasticity of demand for Good X is less than 0.

The income elasticity of demand for Good X is between 0 and 1.

The income elasticity of demand for Good X is greater than 1.

The income elasticity of demand for Good X is equal to 1.

Good X is an inferior good.

The income elasticity of demand for Good X is greater than 1.

Remember that incomce elasticity of demand refers to the percent change in the quantity demanded of a good divided by the percent change in income. Since the percent change in the quantity demanded of Good X was 20% and the percent change in income was 10%, the income elasticity of demand for Good X is 20%/10% = 2. Thus, the income elasticity of demand for Good X is greater than 1.

Good X would be classified as an inferior good only if it had income elasticity of demand less than 0.

Example Question #3 : Microeconomics Graphs

Which of the following statements describes price discrimination?

The price of the same product is the same for different consumers.

The price of two different products are the same for different consumers.

The price of a particular product is less than the marginal cost of producing that product.

The price of two different products are different for different consumers.

The price of the same product is different for different consumers.

The price of the same product is different for different consumers.

Price discrimination occurs when a firm sets two different price levels for different consumers buying the same product. For example, a firm may sell a particular pharmaceutical drug for one price in the US and another price in Europe.

Answer choice "The price of a particular product is less than the marginal cost of producing that product" refers to the rare situation in which a firm sells a good for less than it costs to make it. This may happen in the case of promotions, but is not an example of price discrimination.

The other answer choices represent distortions of the definition of price discrimination and are therefore incorrect.

Example Question #4 : Microeconomics Graphs

Which of the following is true of the relationship between the demand curve and the marginal revenue curve in a monopolistic structure?

The demand curve is always less than or equal to the marginal revenue curve.

The demand curve is always greater than the marginal revenue curve.

The demand curve is always greater than or equal to the marginal revenue curve.

The demand curve is always equal to the marginal revenue curve.

The marginal revenue curve decreases while the demand curve increases.

The demand curve is always greater than or equal to the marginal revenue curve.

A monopolist faces a downward sloping demand curve, indicating market power, in contrast to the horizontal demand curve faced by perfectly competitive firms. A monopolist faces a downward sloping marginal revenue curve as well.

The monopolist's marginal revenue curve has the same y-intercept (intercept on the price-axis) as the demand curve, but has a steeper slope. Therefore, the demand curve is always equal to (at the intercept) or greater than (everywhere after the intercept) the marginal revenue curve. Answer choice "The demand curve is always greater than or equal to the marginal revenue curve" is correct.

The other answer choices are distortions of this relationship.

Example Question #1 : Ap Microeconomics

For a monopolist, marginal cost is equivalent to which of the following?

Average total cost

Industry supply

Average fixed cost

Marginal revenue

Industry supply

Because a monopolist is the only producer in its industry, a monopolist's marginal cost curve is equivalent to the industry supply curve.

Average fixed cost and marginal revenue are incorrect because they are downward sloping, whereas supply is upward sloping.

Average total cost is a distortion of the correct answer.

Example Question #5 : Microeconomics Graphs

Suppose a diseconomy of scale exists for a particular firm. If the firm doubles its output, then ___________.

its short-run average cost will more than double

its long-run average cost will less than double

its long-run average cost will more than double

its short-run average cost will exactly double

its long-run average cost will exactly double

its long-run average cost will more than double

Diseconomies of scale (and economies of scale) refer to the relationship between a firm's output and its long-run average cost. If a firm is operating under a diseconomy of scale, then doubling its output results in more than doubling its long-run average total cost.

Answer choice "its long-run average cost will exactly double" refers to the situation in which the firm is operating at its minimum efficient scale, the lowest point on the long-run average cost curve.

Answer choice "its long-run average cost will less than double" refer to situations in which the firm has an economy of scale.

Answer choices "its short-run average cost will more than double" and "its short-run average cost will exactly double" are incorrect because diseconomies of scale refer to long-run, not short-run, cost curves.

Example Question #6 : Microeconomics Graphs

In order to maximize profits, a firm should continue to produce output until which of the following conditions is met?

Marginal revenue is greater than marginal cost

Total revenue is greater than total cost

Total revenue is equal to marginal revenue

Marginal revenue equals marginal cost

Total cost is equal to total revenue

Marginal revenue equals marginal cost

The profit-maximizing rule for firms is to continue producing until marginal revenue equals marginal cost.

Answer choice "Marginal Revenue is greater than marginal cost" is incorrect, because firms should continue producing under this condition.

All of the other answer choices involving either total revenue or total cost are incorrect because profit-maximization occurs "at the margin", i.e. the profit-maximization rule applies to marginal, not total, cost curves.

Example Question #7 : Microeconomics Graphs

When marginal cost is greater than average total cost, which of the following must be true?

Marginal revenue is equal to marginal cost.

Marginal revenue must be increasing.

Total revenue must be constant.

Average total cost must be increasing.

Average total cost must be decreasing.

Average total cost must be increasing.

We can think of marginal revenue as our grade in a class we are currently taking and average total cost as our total GPA. If we get a better grade in our current class than our GPA, then our GPA must increase. Similarly, if marginal cost is greater than average total cost, then average total cost must be increasing. Answer choice "average total cost must be increasing" is correct.

To eliminate the other answer choices, remember that when marginal cost is greater than average total cost, 1) marginal revenue can still be decreasing, 2) marginal revenue is not necessarily equal to marginal cost, and 3) total revenue can still be changing.

Certified Tutor

All AP Microeconomics Resources